This model is made for learning puposes only and should not be used for investment or decision making.

In this project I implement the almost complete automation of the portfolio optimization and risk using the Markowitz model.

python3 and pip correctly installed

git clone https://github.com/Fnine99/Markowitz_mpt

cd Markowitz_mpt

pip install -r requirements.txt

python3 main.py

Step 1) 5 years monthly price time series data fetching on the Twelve Data API

see data.py

Step 2) Various methods on each assets including:

-Monthly prices

-Monthly returns

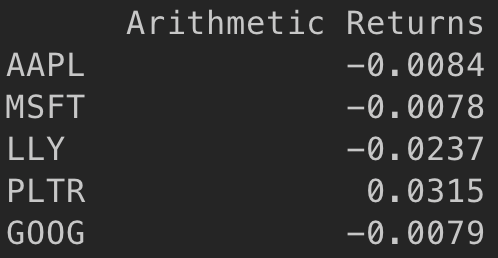

-Arithmetic mean return

-Geometric mean return

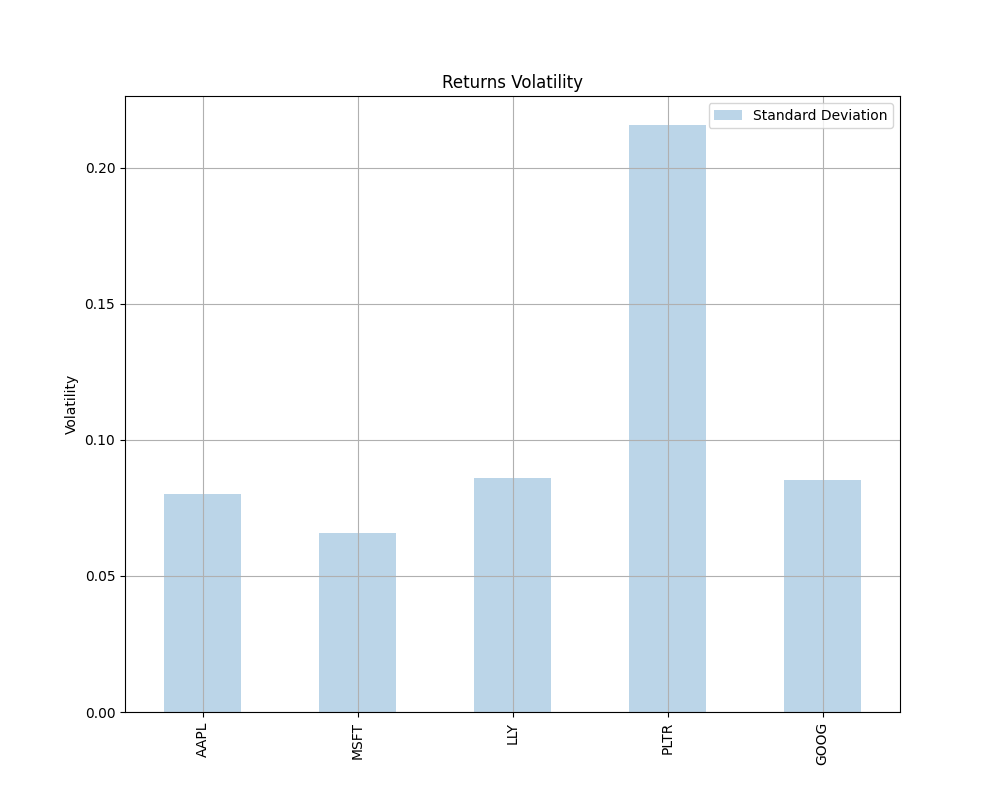

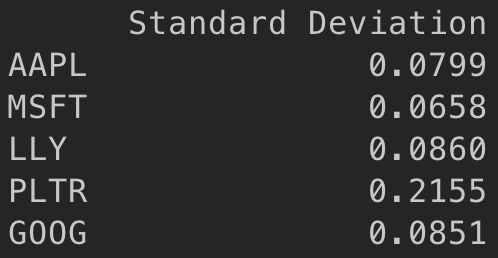

-Monthly returns standard deviation

see assets.py

Step 3) Portfolio construction and Various portfolio methods including:

-Portfolio return

-Porfolio covariance_matrix

-Portfolio variance

-Portfolio standard deviation

-Portfolio correlation matrix

-Portfolio inverse covariance matrix

see portfolio.py

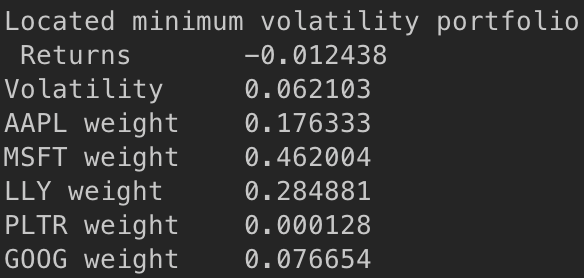

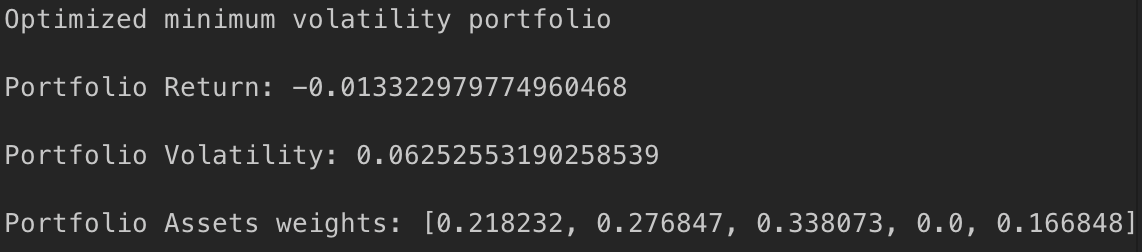

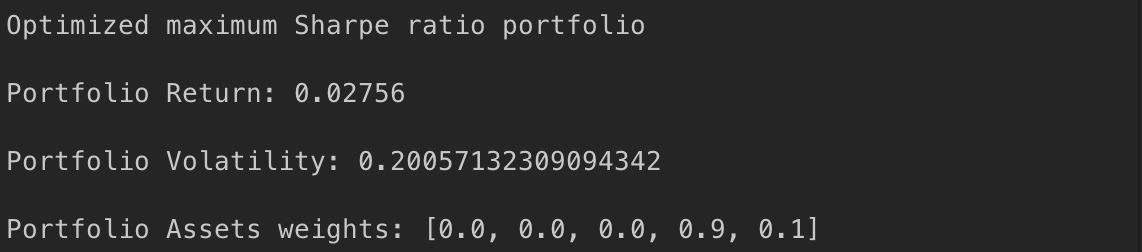

Step 4) Portfolio optimization with Scipy algorithms including finding the assets weights which:

-Minimize the portfolio return

-Maximize the portfolio return

-Minimize the portfolio variance

-Maximize the portfolio variance

-Maximize the portfolio Sharpe ratio

see optimize.py

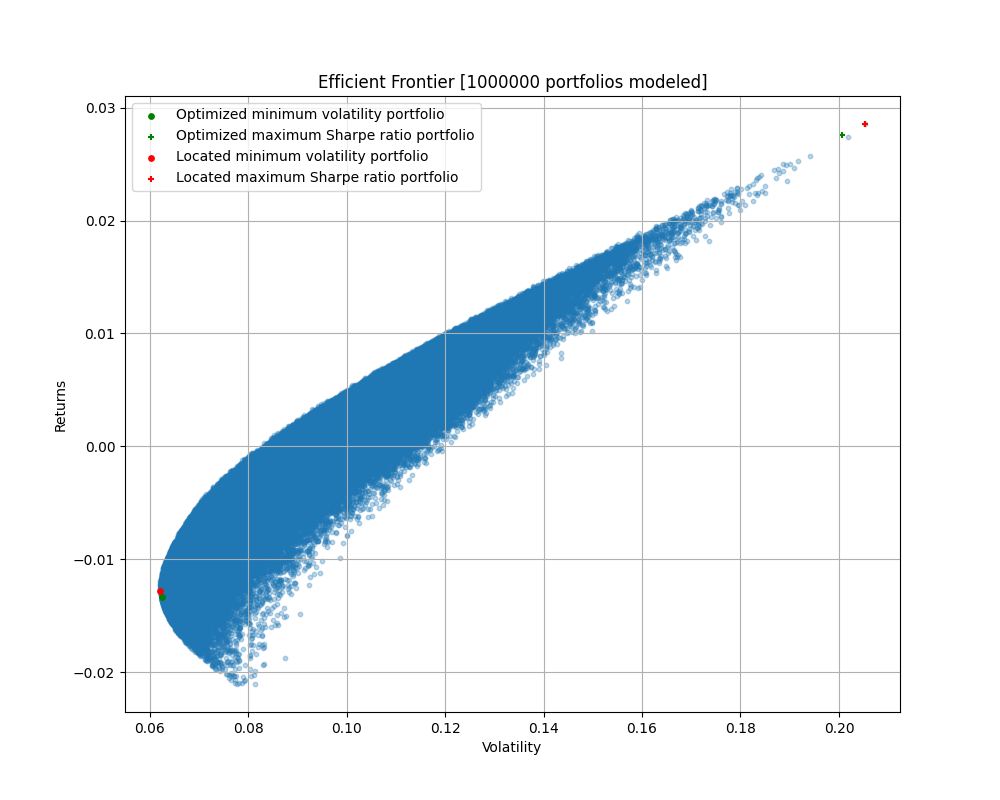

Step 5) Efficient frontier construction and portfolios modelling including:

-Generate X number(1M) of portfolios

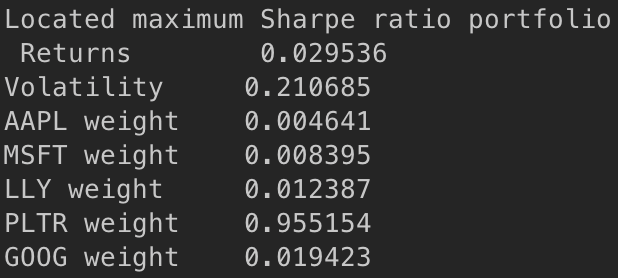

-From those generated portfolios locate the assets weights which:

>Minimize the portfolio variance

>Maximize the portfolio Sharpe ratio

-Plot step 4 and 5

see frontier.py

Step 2:

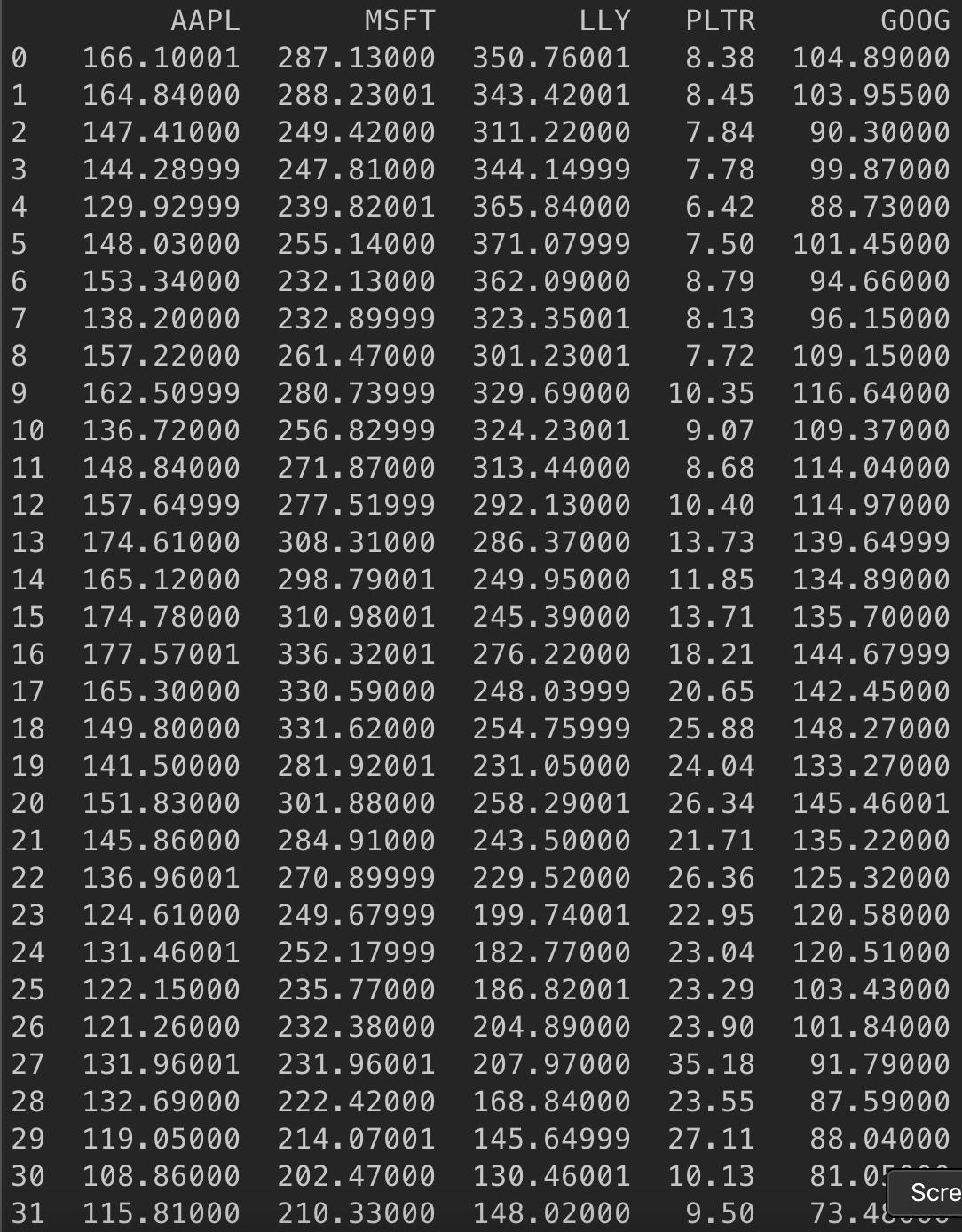

Monthly Prices:

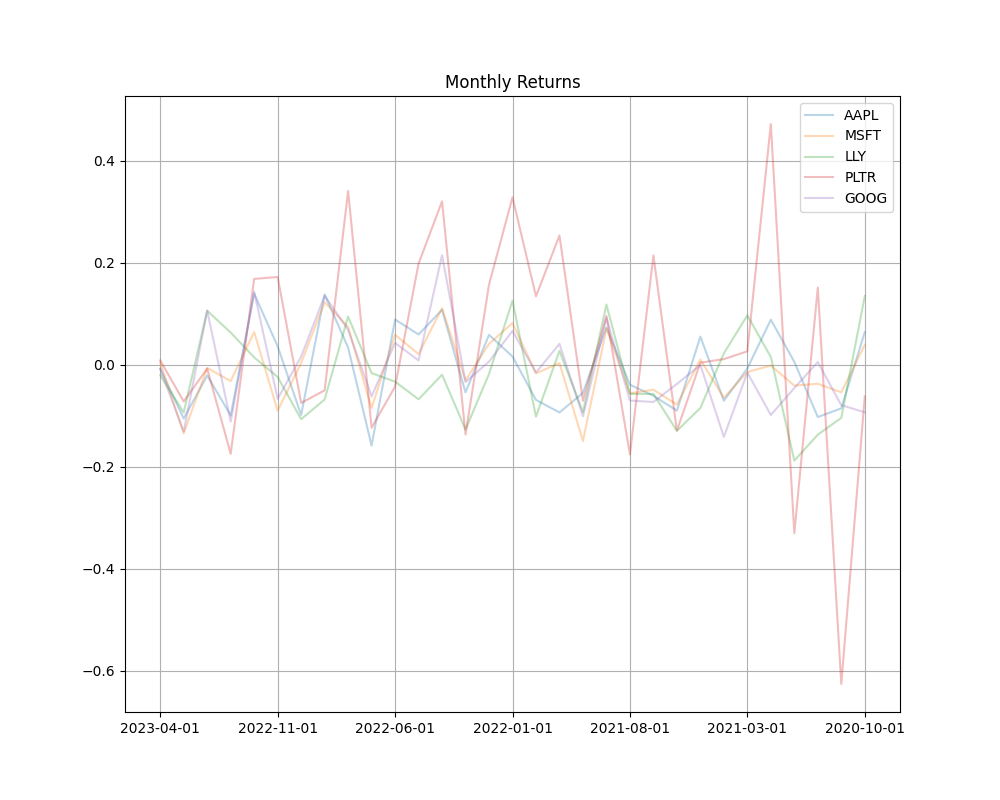

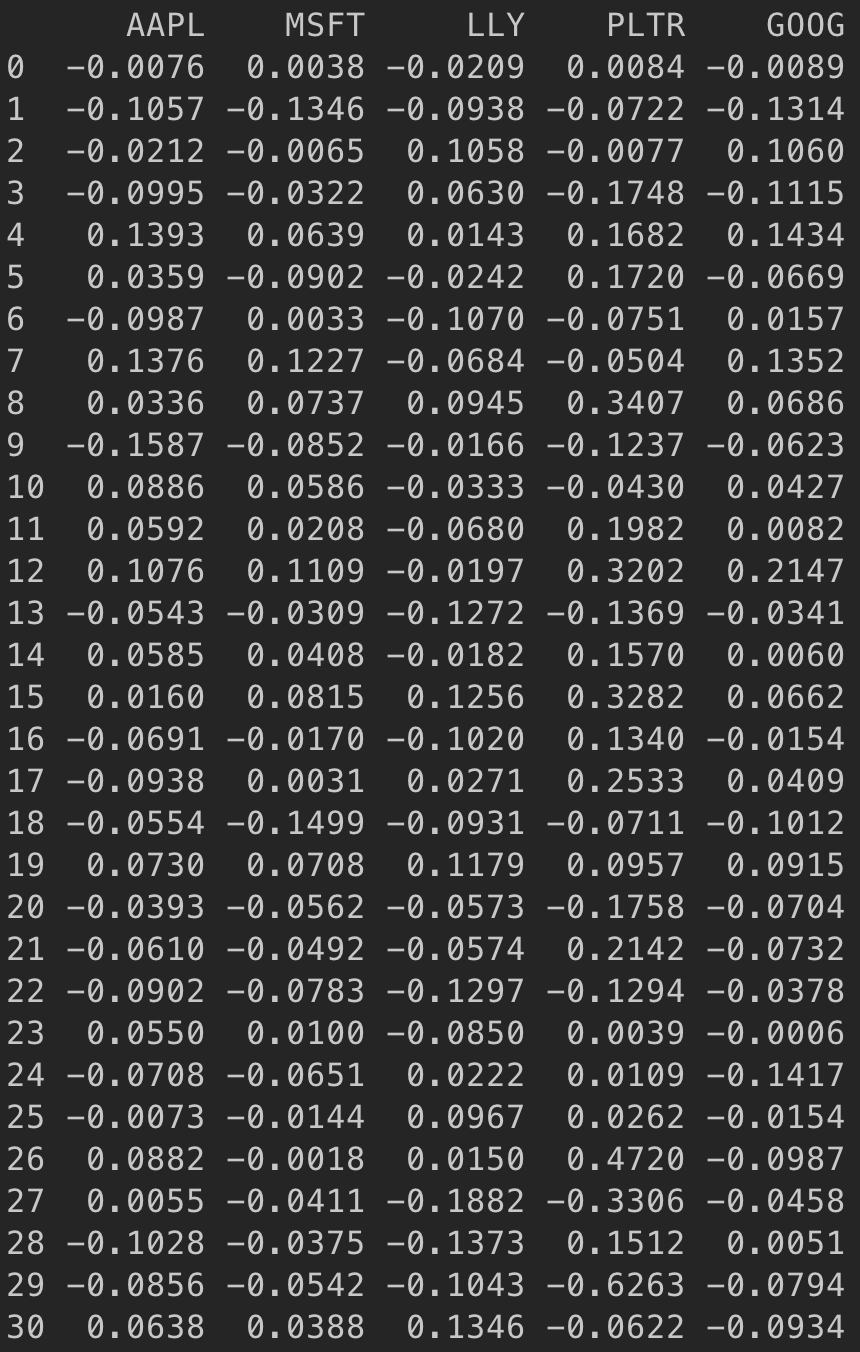

Monthly returns:

Step 3:

Portfolio Covariance Matrix:

Portfolio Correlation Matrix:

Portfolio Inverse Covariance Matrix:

Step 4:

Note that the portfolio with asset weight bounds of [0.000, 0.900] and with a risk-free rate of 0.045. Very interesting to see that, when generating 1M of portfolios, we can very precisely predict the optimized portfolios.

Step 5: